The $\beta(3,2)$ distribution and the # histogram that approximates it.

# #

#

#

#

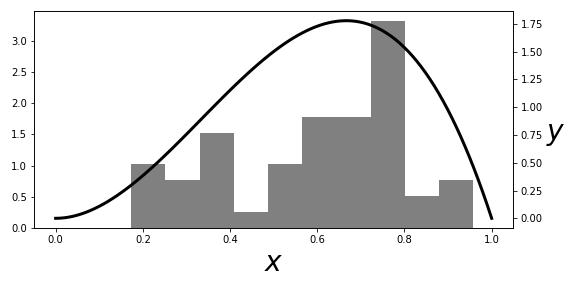

# [Figure](#fig:Bootstrap_001) shows the

# $\beta(3,2)$ distribution and

# the corresponding histogram of the samples. The

# histogram represents

# $\hat{F}$ and is the distribution we sample from to obtain

# the

# bootstrap samples. As shown, the $\hat{F}$ is a pretty crude estimate

# for

# the $F$ density (smooth solid line), but that's not a serious

# problem insofar as

# the following bootstrap estimates are concerned.

# In fact, the approximation

# $\hat{F}$ has a naturally tendency to

# pull towards the bulk of probability mass.

# This is a

# feature, not a bug; and is the underlying mechanism that explains

# bootstrapping, but the formal proofs that exploit this basic

# idea are far out of

# our scope here. The next block generates the

# bootstrap samples

# In[5]:

yboot = np.random.choice(xsamples,(100,50))

yboot_mn = yboot.mean()

# and the bootstrap estimate is therefore,

# In[6]:

np.std(yboot.mean(axis=1)) # approx sqrt(1/1250)

# [Figure](#fig:Bootstrap_002) shows the distribution of computed

# sample means

# from the bootstrap samples. As promised, the next block

# shows how to use

# `sympy.stats` to compute the $\beta(3,2)$ parameters we quoted

# earlier.

# In[7]:

fig,ax = subplots()

fig.set_size_inches(8,4)

_=ax.hist(yboot.mean(axis=1),density=True,color='gray',rwidth=.8)

_=ax.set_title('Bootstrap std of sample mean %3.3f vs actual %3.3f'%

(np.std(yboot.mean(axis=1)),np.sqrt(1/1250.)))

fig.tight_layout()

fig.savefig('fig-statistics/Bootstrap_002.png')

#

#

#

#

#

#

#

#

#

# [Figure](#fig:Bootstrap_001) shows the

# $\beta(3,2)$ distribution and

# the corresponding histogram of the samples. The

# histogram represents

# $\hat{F}$ and is the distribution we sample from to obtain

# the

# bootstrap samples. As shown, the $\hat{F}$ is a pretty crude estimate

# for

# the $F$ density (smooth solid line), but that's not a serious

# problem insofar as

# the following bootstrap estimates are concerned.

# In fact, the approximation

# $\hat{F}$ has a naturally tendency to

# pull towards the bulk of probability mass.

# This is a

# feature, not a bug; and is the underlying mechanism that explains

# bootstrapping, but the formal proofs that exploit this basic

# idea are far out of

# our scope here. The next block generates the

# bootstrap samples

# In[5]:

yboot = np.random.choice(xsamples,(100,50))

yboot_mn = yboot.mean()

# and the bootstrap estimate is therefore,

# In[6]:

np.std(yboot.mean(axis=1)) # approx sqrt(1/1250)

# [Figure](#fig:Bootstrap_002) shows the distribution of computed

# sample means

# from the bootstrap samples. As promised, the next block

# shows how to use

# `sympy.stats` to compute the $\beta(3,2)$ parameters we quoted

# earlier.

# In[7]:

fig,ax = subplots()

fig.set_size_inches(8,4)

_=ax.hist(yboot.mean(axis=1),density=True,color='gray',rwidth=.8)

_=ax.set_title('Bootstrap std of sample mean %3.3f vs actual %3.3f'%

(np.std(yboot.mean(axis=1)),np.sqrt(1/1250.)))

fig.tight_layout()

fig.savefig('fig-statistics/Bootstrap_002.png')

#

#

#

#

# For each bootstrap draw, we compute the sample # mean. This is the histogram of those sample means that will be used to compute # the bootstrap estimate of the standard deviation.

# #

#

# In[8]:

import sympy as S

import sympy.stats

for i in range(50): # 50 samples

# load sympy.stats Beta random variables

# into global namespace using exec

execstring = "x%d = S.stats.Beta('x'+str(%d),3,2)"%(i,i)

exec(execstring)

# populate xlist with the sympy.stats random variables

# from above

xlist = [eval('x%d'%(i)) for i in range(50) ]

# compute sample mean

sample_mean = sum(xlist)/len(xlist)

# compute expectation of sample mean

sample_mean_1 = S.stats.E(sample_mean).evalf()

# compute 2nd moment of sample mean

sample_mean_2 = S.stats.E(S.expand(sample_mean**2)).evalf()

# standard deviation of sample mean

# use sympy sqrt function

sigma_smn = S.sqrt(sample_mean_2-sample_mean_1**2) # sqrt(2)/50

print(sigma_smn)

# **Programming Tip.**

#

# Using the `exec` function enables the creation of a

# sequence of Sympy

# random variables. Sympy has the `var` function which can

# automatically

# create a sequence of Sympy symbols, but there is no corresponding

# function in the statistics module to do this for random variables.

#

#

#

#

#

#

#

# **Example.** Recall the delta method

# from the section [sec:delta_method](#sec:delta_method). Suppose we have a set

# of Bernoulli coin-flips

# ($X_i$) with probability of head $p$. Our maximum

# likelihood estimator

# of $p$ is $\hat{p}=\sum X_i/n$ for $n$ flips. We know this

# estimator

# is unbiased with $\mathbb{E}(\hat{p})=p$ and $\mathbb{V}(\hat{p}) =

# p(1-p)/n$. Suppose we want to use the data to estimate the variance of

# the

# Bernoulli trials ($\mathbb{V}(X)=p(1-p)$). By the notation the

# delta method,

# $g(x) = x(1-x)$. By the plug-in principle, our maximum

# likelihood estimator of

# this variance is then $\hat{p}(1-\hat{p})$. We

# want the variance of this

# quantity. Using the results of the delta

# method, we have

#

# $$

# \begin{align*}

# \mathbb{V}(g(\hat{p})) &=(1-2\hat{p})^2\mathbb{V}(\hat{p})

# \\\

# \mathbb{V}(g(\hat{p})) &=(1-2\hat{p})^2\frac{\hat{p}(1-\hat{p})}{n} \\\

# \end{align*}

# $$

#

# Let's see how useful this is with a short simulation.

# In[9]:

import numpy as np

np.random.seed(123)

# In[10]:

from scipy import stats

import numpy as np

p= 0.25 # true head-up probability

x = stats.bernoulli(p).rvs(10)

print(x)

# The maximum likelihood estimator of $p$ is $\hat{p}=\sum X_i/n$,

# In[11]:

phat = x.mean()

print(phat)

# Then, plugging this into the delta method approximant above,

# In[12]:

print((1-2*phat)**2*(phat)**2/10)

# Now, let's try this using the bootstrap estimate of the variance

# In[13]:

phat_b=np.random.choice(x,(50,10)).mean(1)

print(np.var(phat_b*(1-phat_b)))

# This shows that the delta method's estimated variance

# is different from the

# bootstrap method, but which one is better?

# For this situation we can solve for

# this directly using Sympy

# In[14]:

import sympy as S

from sympy.stats import E, Bernoulli

xdata =[Bernoulli(i,p) for i in S.symbols('x:10')]

ph = sum(xdata)/float(len(xdata))

g = ph*(1-ph)

# **Programming Tip.**

#

# The argument in the `S.symbols('x:10')` function returns a

# sequence of Sympy

# symbols named `x1,x2` and so on. This is shorthand for

# creating and naming each

# symbol sequentially.

#

#

#

# Note that `g` is the

# $g(\hat{p})=\hat{p}(1- \hat{p})$

# whose variance we are trying to estimate.

# Then,

# we can plug in for the estimated $\hat{p}$ and get the correct

# value for

# the variance,

# In[15]:

print(E(g**2) - E(g)**2)

# This case is generally representative --- the delta method tends

# to

# underestimate the variance and the bootstrap estimate is better here.

#

#

# ## Parametric Bootstrap

#

# In the previous example, we used the $\lbrace x_1, x_2,

# \ldots, x_n \rbrace $

# samples themselves as the basis for $\hat{F}$ by weighting

# each with $1/n$. An

# alternative is to *assume* that the samples come from a

# particular

# distribution, estimate the parameters of that distribution from the

# sample set,

# and then use the bootstrap mechanism to draw samples from the

# assumed

# distribution, using the so-derived parameters. For example, the next

# code block

# does this for a normal distribution.

# In[19]:

n = 100

rv = stats.norm(0,2)

xsamples = rv.rvs(n)

# estimate mean and var from xsamples

mn_ = np.mean(xsamples)

std_ = np.std(xsamples)

# bootstrap from assumed normal distribution with

# mn_,std_ as parameters

rvb = stats.norm(mn_,std_) #plug-in distribution

yboot = rvb.rvs((n,500)).var(axis=0)

#

#

# Recall

# the sample variance estimator is the following:

#

# $$

# S^2 = \frac{1}{n-1} \sum (X_i-\bar{X})^2

# $$

#

# Assuming that the samples are normally distributed, this

# means that

# $(n-1)S^2/\sigma^2$ has a chi-squared distribution with

# $n-1$ degrees of

# freedom. Thus, the variance, $\mathbb{V}(S^2) = 2

# \sigma^4/(n-1) $. Likewise,

# the MLE plug-in estimate for this is

# $\mathbb{V}(S^2) = 2 \hat{\sigma}^4/(n-1)$

# The following code computes

# the variance of the sample variance, $S^2$ using the

# MLE and bootstrap

# methods.

# In[20]:

# MLE-Plugin Variance of the sample mean

print(2*std_**4/(n-1)) # MLE plugin

# Bootstrap variance of the sample mean

print(yboot.var())

# True variance of sample mean

print(2*(2**4)/(n-1))

#

#

# This

# shows that the bootstrap estimate is better here than the MLE

# plugin estimate.

# Note that this technique becomes even more powerful with multivariate

# distributions with many parameters because all the mechanics are the same.

# Thus,

# the bootstrap is a great all-purpose method for computing standard

# errors, but,

# in the limit, is it converging to the correct value? This is the

# question of

# *consistency*. Unfortunately, to answer this question requires more

# and deeper

# mathematics than we can get into here. The short answer is that for

# estimating

# standard errors, the bootstrap is a consistent estimator in a wide

# range of

# cases and so it definitely belongs in your toolkit.

#

#

# In[8]:

import sympy as S

import sympy.stats

for i in range(50): # 50 samples

# load sympy.stats Beta random variables

# into global namespace using exec

execstring = "x%d = S.stats.Beta('x'+str(%d),3,2)"%(i,i)

exec(execstring)

# populate xlist with the sympy.stats random variables

# from above

xlist = [eval('x%d'%(i)) for i in range(50) ]

# compute sample mean

sample_mean = sum(xlist)/len(xlist)

# compute expectation of sample mean

sample_mean_1 = S.stats.E(sample_mean).evalf()

# compute 2nd moment of sample mean

sample_mean_2 = S.stats.E(S.expand(sample_mean**2)).evalf()

# standard deviation of sample mean

# use sympy sqrt function

sigma_smn = S.sqrt(sample_mean_2-sample_mean_1**2) # sqrt(2)/50

print(sigma_smn)

# **Programming Tip.**

#

# Using the `exec` function enables the creation of a

# sequence of Sympy

# random variables. Sympy has the `var` function which can

# automatically

# create a sequence of Sympy symbols, but there is no corresponding

# function in the statistics module to do this for random variables.

#

#

#

#

#

#

#

# **Example.** Recall the delta method

# from the section [sec:delta_method](#sec:delta_method). Suppose we have a set

# of Bernoulli coin-flips

# ($X_i$) with probability of head $p$. Our maximum

# likelihood estimator

# of $p$ is $\hat{p}=\sum X_i/n$ for $n$ flips. We know this

# estimator

# is unbiased with $\mathbb{E}(\hat{p})=p$ and $\mathbb{V}(\hat{p}) =

# p(1-p)/n$. Suppose we want to use the data to estimate the variance of

# the

# Bernoulli trials ($\mathbb{V}(X)=p(1-p)$). By the notation the

# delta method,

# $g(x) = x(1-x)$. By the plug-in principle, our maximum

# likelihood estimator of

# this variance is then $\hat{p}(1-\hat{p})$. We

# want the variance of this

# quantity. Using the results of the delta

# method, we have

#

# $$

# \begin{align*}

# \mathbb{V}(g(\hat{p})) &=(1-2\hat{p})^2\mathbb{V}(\hat{p})

# \\\

# \mathbb{V}(g(\hat{p})) &=(1-2\hat{p})^2\frac{\hat{p}(1-\hat{p})}{n} \\\

# \end{align*}

# $$

#

# Let's see how useful this is with a short simulation.

# In[9]:

import numpy as np

np.random.seed(123)

# In[10]:

from scipy import stats

import numpy as np

p= 0.25 # true head-up probability

x = stats.bernoulli(p).rvs(10)

print(x)

# The maximum likelihood estimator of $p$ is $\hat{p}=\sum X_i/n$,

# In[11]:

phat = x.mean()

print(phat)

# Then, plugging this into the delta method approximant above,

# In[12]:

print((1-2*phat)**2*(phat)**2/10)

# Now, let's try this using the bootstrap estimate of the variance

# In[13]:

phat_b=np.random.choice(x,(50,10)).mean(1)

print(np.var(phat_b*(1-phat_b)))

# This shows that the delta method's estimated variance

# is different from the

# bootstrap method, but which one is better?

# For this situation we can solve for

# this directly using Sympy

# In[14]:

import sympy as S

from sympy.stats import E, Bernoulli

xdata =[Bernoulli(i,p) for i in S.symbols('x:10')]

ph = sum(xdata)/float(len(xdata))

g = ph*(1-ph)

# **Programming Tip.**

#

# The argument in the `S.symbols('x:10')` function returns a

# sequence of Sympy

# symbols named `x1,x2` and so on. This is shorthand for

# creating and naming each

# symbol sequentially.

#

#

#

# Note that `g` is the

# $g(\hat{p})=\hat{p}(1- \hat{p})$

# whose variance we are trying to estimate.

# Then,

# we can plug in for the estimated $\hat{p}$ and get the correct

# value for

# the variance,

# In[15]:

print(E(g**2) - E(g)**2)

# This case is generally representative --- the delta method tends

# to

# underestimate the variance and the bootstrap estimate is better here.

#

#

# ## Parametric Bootstrap

#

# In the previous example, we used the $\lbrace x_1, x_2,

# \ldots, x_n \rbrace $

# samples themselves as the basis for $\hat{F}$ by weighting

# each with $1/n$. An

# alternative is to *assume* that the samples come from a

# particular

# distribution, estimate the parameters of that distribution from the

# sample set,

# and then use the bootstrap mechanism to draw samples from the

# assumed

# distribution, using the so-derived parameters. For example, the next

# code block

# does this for a normal distribution.

# In[19]:

n = 100

rv = stats.norm(0,2)

xsamples = rv.rvs(n)

# estimate mean and var from xsamples

mn_ = np.mean(xsamples)

std_ = np.std(xsamples)

# bootstrap from assumed normal distribution with

# mn_,std_ as parameters

rvb = stats.norm(mn_,std_) #plug-in distribution

yboot = rvb.rvs((n,500)).var(axis=0)

#

#

# Recall

# the sample variance estimator is the following:

#

# $$

# S^2 = \frac{1}{n-1} \sum (X_i-\bar{X})^2

# $$

#

# Assuming that the samples are normally distributed, this

# means that

# $(n-1)S^2/\sigma^2$ has a chi-squared distribution with

# $n-1$ degrees of

# freedom. Thus, the variance, $\mathbb{V}(S^2) = 2

# \sigma^4/(n-1) $. Likewise,

# the MLE plug-in estimate for this is

# $\mathbb{V}(S^2) = 2 \hat{\sigma}^4/(n-1)$

# The following code computes

# the variance of the sample variance, $S^2$ using the

# MLE and bootstrap

# methods.

# In[20]:

# MLE-Plugin Variance of the sample mean

print(2*std_**4/(n-1)) # MLE plugin

# Bootstrap variance of the sample mean

print(yboot.var())

# True variance of sample mean

print(2*(2**4)/(n-1))

#

#

# This

# shows that the bootstrap estimate is better here than the MLE

# plugin estimate.

# Note that this technique becomes even more powerful with multivariate

# distributions with many parameters because all the mechanics are the same.

# Thus,

# the bootstrap is a great all-purpose method for computing standard

# errors, but,

# in the limit, is it converging to the correct value? This is the

# question of

# *consistency*. Unfortunately, to answer this question requires more

# and deeper

# mathematics than we can get into here. The short answer is that for

# estimating

# standard errors, the bootstrap is a consistent estimator in a wide

# range of

# cases and so it definitely belongs in your toolkit.